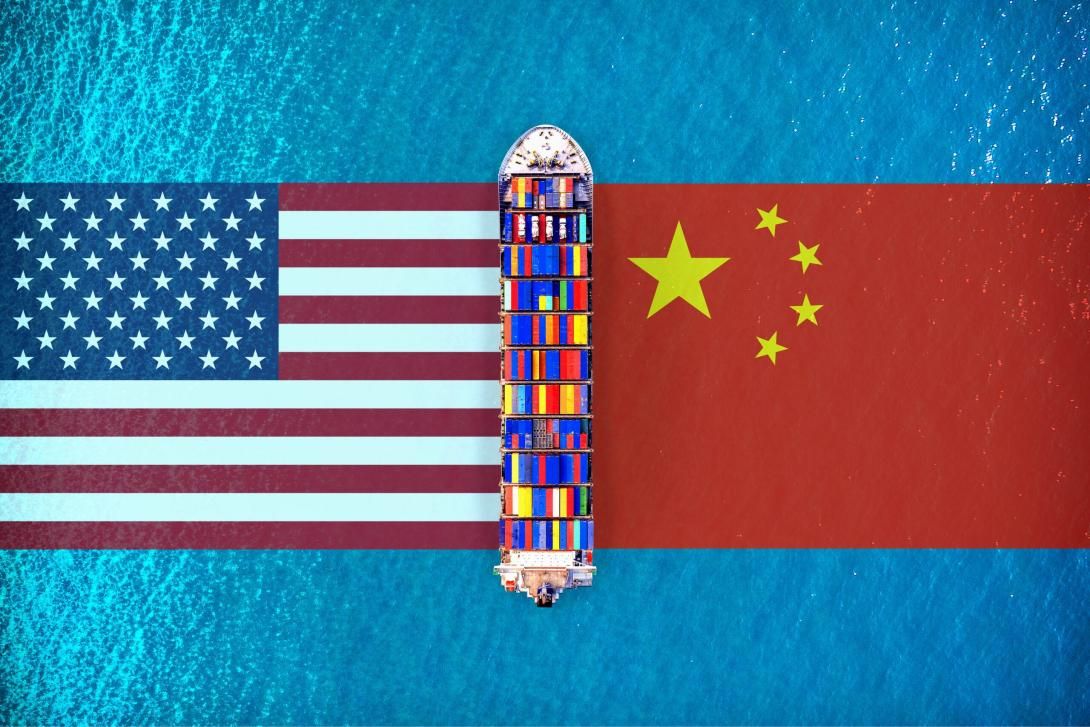

US-China: the trade war that will define the future

The perfect storm has been about to shake up the global trade board this October. China and the United States have once again crossed a red line with restrictions on rare earths and 100% tariffs, threatening not only bilateral relations but the future of strategic sectors: semiconductors, maritime transport, electric vehicles. What is at stake is not only trade, but who will lead technological innovation and the energy transition of the 21st century. The one-year agreement reached in Busan, Korea at the end of the month, has suspended the catastrophic effects on global trade and maritime transport that this new escalation was causing.

Jordi Torrent is the Strategy Manager at Port de Barcelona.

Published on 14/10/2025

Share

The trade clash between Washington and Beijing reaches new highs in October 2025 with 100% tariffs and rare earth restrictions. (FP)

Tensions between the US and China have nearly caused a very turbulent autumn for international trade and global supply chains. Especially in the already battered transpacific relationship that has accumulated several semesters of disruptions. The trade war, initially driven by Donald Trump, continued by Biden, and which China does not hesitate to respond to, seeks, on one hand, to break US commercial dependence on the Asian giant. On the other, with their trade measures, both countries aim to lead the transition to the digital and green economy.

Chinese restrictions on rare earth eports

After several months of calm in the China-US relationship, the first week of October saw torrential rains fall again on the game board between both powers. China announced new restrictions on rare earth exports, to which Trump responded by announcing a 100% increase in tariffs on Chinese exports to the US, set to take effect on November 1st.

The resurgence of the trade war between the two global giants pushed American stock markets down. Wall Street can't catch a break. As a consequence of the new confrontation, the meeting initially scheduled for late October between Trump and Xi Jinping it seemed it was not going to take place.

How are these restrictions explained?

The restrictions on rare earth exports by China had been a response to previous limitations imposed by Trump on chip exports to the Asian giant.

Two apparently irreconcilable positions coexist within the Trump administration regarding the technological relationship with China:

some believe that breaking exchanges with their geostrategic rival will limit the development of artificial intelligence and China's digital economy.

others consider that it causes precisely the opposite: driving and consolidating an independent national sector separate from the American ecosystem on which it still depends in some, but increasingly fewer, sectors. For them, it would be preferable to maintain technological exchanges (for example, by promoting the export of Nvidia semiconductors) so that China continues to depend on American innovation and technological advances.

But this does not appear to be the dominant position right now in the US Department of Commerce. The anti-Chinese hawks of the American administration, led by Peter Navarro, seemed to have won the battle. Commerce Secretary Howard Lutnick, apparently less intransigent and experienced in the complexities of the financial world on Wall Street, has quickly become imbued with the simplistic anti-China rhetoric predominant in official discourse.

Imagen

The trade confrontation between the US and China directly impacts ports and international maritime transport, where more than 80% of global trade is concentrated. (FP)

Made in China 2025

In fact, the US seeks to avoid what has happened in the last decade with the 17 rare earths of which China is already the world's leading refiner and which, allowing for differences, are to the digital economy, military industry, and AI what oil is to manufacturing and transportation.

The Communist Party had set a goal to be self-sufficient and, after years of planning, has achieved the objective it had set for itself as part of Made in China 2025.

It has also achieved this with helium, on which it was extremely dependent on the US. It has gone from importing more than 90% of it from the United States to less than 10%. Now, Russia and Persian Gulf countries, among others, are its main suppliers. Once sovereignty has been achieved in this last area, there is practically no segment in which it depends on the Americans.

Imagen

The "Made in China 2025" program has enabled the Asian giant to achieve self-sufficiency in critical technologies for AI, the digital economy, and the military industry. (FP)

Fines for shipping companies

This month of October brought us new shocks with unpredictable medium-term consequences. On October 14th, fines came into effect for shipping companies that call at US ports with ships built in China, whose shipyards produce more than half of the world's merchant fleet.

Chinese shipowners, especially the state-owned company Cosco, were the ones who suffered the most from the impact of the penalties, but almost all the major global groups were affected to a greater or lesser extent. Trump aimed with this to recover merchant ship production in depressed American shipyards. A very difficult objective, after decades of abandonment of the shipbuilding sector, no matter how many fines are imposed on ships built in China.

The extraordinary innovation that this sector has experienced in the 21st century is primarily the patrimony of the Chinese and Koreans and will hardly be transferable and internalized in shipyards where a cargo vessel hasn't been built since the last century.

Imagen

The sea, stage of confrontation: while China dominates global shipbuilding, the US attempts to revive its shipyards with protectionist measures. (FP)

Transport decarbonization

The energy transition and transport decarbonization also pit the two giants against each other. While China has decisively bet on the transition to electric vehicles in the passenger transport sector, Trump, with the exception of the Tesla brand, represents a brake on the transformation of aging American automobile production toward electric vehicles.

While in Chinese megalopolises electric vehicles approach the majority (which has allowed the eternal gray horizons resulting from pollution to give way to seeing the blue sky again), in many places in the US, huge pickups with fuel consumption from another era continue to dominate the roads.

Zero emissions in maritime transport: NZF

Something similar could be happening in the maritime transport sector. October has also been a decisive month in this regard. Mid-month, at the International Maritime Organization (IMO) meeting, the NZF (the net-zero framework) was to be voted on, whose objective is to contribute to the decarbonization of maritime transport through the imposition of penalties on shipowners and vessels based on their greenhouse gas emissions.

Trump had announced that the US would vote against it and threatened reprisals against countries that voted in favor. China, like most IMO member countries, had announced its intention to vote in favor of the proposal. Finally, Trump, with the invaluable help of Saudi Arabia and some leading flag states, managed to suspend the approval of the NZF for at least one year.

Imagen

Más allá de aranceles y semiconductores: la confrontación EEUU-China tiene una creciente dimensión militar centrada en el estrecho de Taiwán. (FP)

Sale of international terminals and Taiwan

It is also unlikely that this autumn will see progress in the sale of international terminals of the Chinese group Hutchison, sponsored by Trump and blocked by the Asian country's competition authorities, one of whose objectives was to remove the Hong Kong-based company from the management of container terminals in the strategic Panama Canal.

The October storm could turn into a hurricane, with its epicenter in Taiwan, as a consequence of the military and verbal escalation of recent days between China, the island, and the US. The investigation launched by China, which includes substantial rewards, on several citizens of the island accused of promoting separatism, does not seem to be heading in the right direction.

Imagen

Trump and Xi Jinping in Busan, Korea, on October 30. (The White House)

The Agreement in Busan, Korea

Finally, after weeks of great tension, Xi Jinping and Donald Trump signed a new truce (we'll see if it's definitive) in their trade war in Busan, Korea on October 30. Everything seems to indicate that, despite the pressure from the anti-China hawks in his administration, other more sensible and realistic voices have prevailed. The agreement, in fact, was more necessary for the US than for China, which has already managed to reduce the weight of its exports to the US below 10%. On the other hand, American companies, especially technology, military and automotive ones, are absolutely dependent on the rare earths that are refined in China and of which it is the main (and in some cases, only) global supplier.

Imagen

The possible reopening of the Red Sea route would further facilitate access of Asian products to the European market, the main alternative to the US market. (FP)

How it will affect container volumes in mediterranean ports

This end of year could bring other good news. If the ceasefire in Gaza holds, the Houthi attacks on navigation in the Red Sea will presumably soon cease as well, which would lead to the return of maritime transport, especially containers, to the traditional route linking Asia with Europe through Suez.

In the last two years, Chinese shipowners, unlike Western ones, have been able to navigate the Red Sea with a little more freedom. Abandoning the route through the Cape of Good Hope will reduce transit times between Asia and Europe and will also cause fluctuations in the volumes of containers handled in Spanish Mediterranean ports in favor of those located near Suez and in North Africa.

The return to the Red Sea will further facilitate access of Asian products, especially Chinese, to the European market. These will continue seeking an alternative to the American market, subject to Donald Trump's tariff fluctuations, and the EU, after its own internal market, remains the natural destination for Chinese merchandise exports for consumption by the global middle class.