Charging stations for electric vehicles in China. [Image: WangAnQi / Getty]

Charging stations for electric vehicles in China. [Image: WangAnQi / Getty]

China Takes Control Of The Electric Vehicle

The pressure to cut contamination from private vehicles is mounting and electric cars seem to be the most viable alternative to this global issue. China has taken the lead, not only in terms of global production of the finished product but also in batteries and raw materials used for manufacturing. Where does this leave Europe and the United States in terms of leading this industry of the future? Here are some keys to the new map of power and interests regarding the electric vehicle.

Posted on

09.02.2018

Carlos Martín is the Manager of the Ports and Maritime Transport Consultancy Area at IDOM.

Charging stations for electric vehicles in China. [Image: WangAnQi / Getty]

China has positioned itself as the one to beat, willing to take control of the production and sale of electric cars, leaving Europe and the United States a distant second. Its strategy combines private initiatives from battery and car makers with financial and strategic backing from the government, which for 5 years now has been pushing an ambitious plan to transform the status quo in the automotive sector and the associated foreign trade relations, which encompass both raw materials for batteries and electric vehicles as well as the finished product.

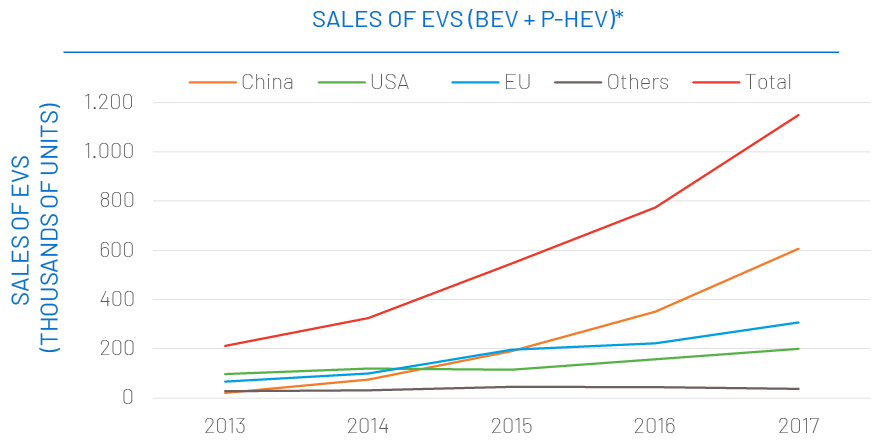

China is now the leading producer and commercialiser of electric vehicles. According to the China Association of Automobile Manufacturers, 680,000 light electric vehicles were manufactured in the country in 2017, plus 198,000 commercial electric vehicles, making it the number one manufacturer in the world. Since 2013, when China produced 23,700 electric cars, the industry in this Asian giant has seen year-on-year growth of 692%.

Light vehicles only. Heavy vehicles not included. Source: EV Volumes (The Electric World Sales Database) and CAAM (China Association Of Automoblie Manufacturers).

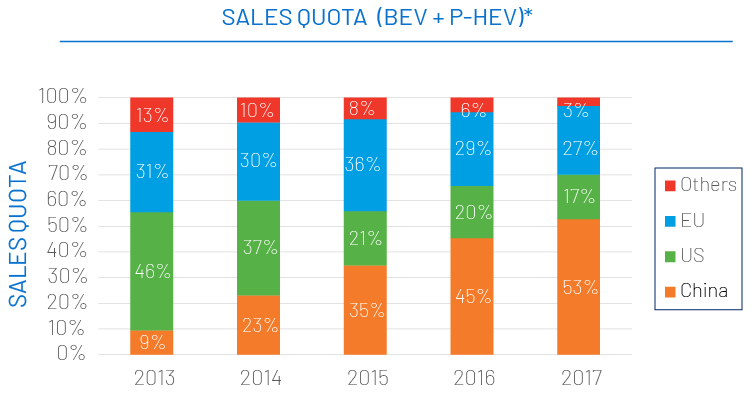

Plus, 606,000 electric vehicles made in China were sold in 2017, which accounts for 53% of the global market. Since 2013, the Chinese market has seen year-on-year growth of 733%. In 2014, China was already positioned as the top commercialiser of electric vehicles in the world, ahead of Europe and the United States. China's yearly growth, at a pace that its competitors can't keep up with, is down to several causes. Firstly, Chinese manufacturers are backed by the significant captive demand inside this Asian country. Plus, not only is the total volume of vehicles manufactured increasing, so is the range of models on offer. In 2017, Chinese buyers had 75 models of electric vehicles to choose from, more than in any other country.

* Light vehicles only. Heavy vehicles not included. Source: EV Volumes (The Electric World Sales Database) and CAAM (China Association Of Automoblie Manufacturers).

The Chinese government is responsible for both encouraging new models and incentivising demand, with subsidies covering up to 23% of the vehicle purchase price; tax and licensing breaks; and income tax deductions. Plus, the administration is investing in recharging facilities to make it easier to use electric vehicles. In 2016, China had a network of 107,000 charging points.

Batteries and power

The main limitation on the electric car market is the cost of batteries, which is about 30% of the vehicle price. Asian manufacturers have positioned themselves as leaders in producing and commercialising Li-Ion batteries. China, South Korea and Japan have 8 of the top 10 battery manufacturers in the world, which in 2016 were responsible for more than 85% of production worldwide. Specifically, there are 3 Chinese manufacturers among the top 5, including the number one company: CATL. In 2016, Chinese manufacturers produced more than 25% of the global capacity; in 2017 that figure was 55% and it is expected to be more than 63% by 2021. In 2016, there were 140 manufacturers of Li-Ion batteries in China.

90% of electric vehicles manufactured in China used batteries from Chinese producers. [Image of Mikes Photos]